Tax residency in Singapore has always been more than a legal definition — it is a decisive factor that shapes how individuals and companies are taxed, what reliefs they can claim, and whether they can access Singapore’s extensive network of double taxation agreements (DTAs). In 2025, as international standards on tax transparency tighten and the Inland Revenue Authority of Singapore (IRAS) refines its guidance, understanding the criteria and securing residency status has never been more critical.

This article provides a complete guide to the rules, practical tips, and common pitfalls for both individuals and companies aiming to qualify as tax residents in Singapore.

This article provides a complete guide to the rules, practical tips, and common pitfalls for both individuals and companies aiming to qualify as tax residents in Singapore.

Why Tax Residency Matters

The consequences of being classified as a tax resident or a non-resident in Singapore are substantial. Residents are taxed on a progressive scale, enjoy reliefs and exemptions, and often benefit from lower overall liabilities. Non-residents, by contrast, face flat rates, have limited access to deductions, and cannot rely on treaty protection.

For companies, tax residency can determine whether foreign-sourced income is exempt, whether withholding tax relief is available under Singapore’s 90+ DTAs, and ultimately, whether the group structure is competitive in global markets. In an era of BEPS 2.0 and heightened scrutiny of “substance,” residency is a strategic status — not a box-ticking exercise.

For companies, tax residency can determine whether foreign-sourced income is exempt, whether withholding tax relief is available under Singapore’s 90+ DTAs, and ultimately, whether the group structure is competitive in global markets. In an era of BEPS 2.0 and heightened scrutiny of “substance,” residency is a strategic status — not a box-ticking exercise.

Individual Tax Residency in 2025

The 183-Day Rule and Administrative Concessions

For individuals, the most straightforward test is the 183-day rule: spending at least 183 days in Singapore during a calendar year typically secures tax residency.

IRAS also applies two important concessions:

Singapore citizens and permanent residents who ordinarily reside in Singapore are also considered residents, unless their absence is substantial and permanent.

Residents vs Non-Residents

Practical Considerations

Counting days accurately is vital, including short absences for travel, which IRAS often treats as part of continuous presence. Maintaining evidence of residence — leases, utility bills, dependent family members — strengthens the case. For those seeking treaty benefits in another jurisdiction, applying for a Certificate of Residence (COR) is essential.

For individuals, the most straightforward test is the 183-day rule: spending at least 183 days in Singapore during a calendar year typically secures tax residency.

IRAS also applies two important concessions:

- The Two-Year Rule: if employment straddles two years and the total stay is at least 183 days, the individual is treated as a resident for both years.

- The Three-Year Rule: a continuous period of employment covering three consecutive years results in residency throughout, even if the first or last year includes fewer than 183 days.

Singapore citizens and permanent residents who ordinarily reside in Singapore are also considered residents, unless their absence is substantial and permanent.

Residents vs Non-Residents

- Residents: taxed at progressive rates from 0% to 24%, with eligibility for personal reliefs and deductions. Most foreign income is exempt unless remitted, and exemptions apply to specified dividends, branch profits, and service income.

- Non-residents: taxed at 15% or resident rates (whichever is higher) on employment income; other fees such as director’s remuneration and consultancy income are taxed at 24%. They cannot claim most reliefs.

Practical Considerations

Counting days accurately is vital, including short absences for travel, which IRAS often treats as part of continuous presence. Maintaining evidence of residence — leases, utility bills, dependent family members — strengthens the case. For those seeking treaty benefits in another jurisdiction, applying for a Certificate of Residence (COR) is essential.

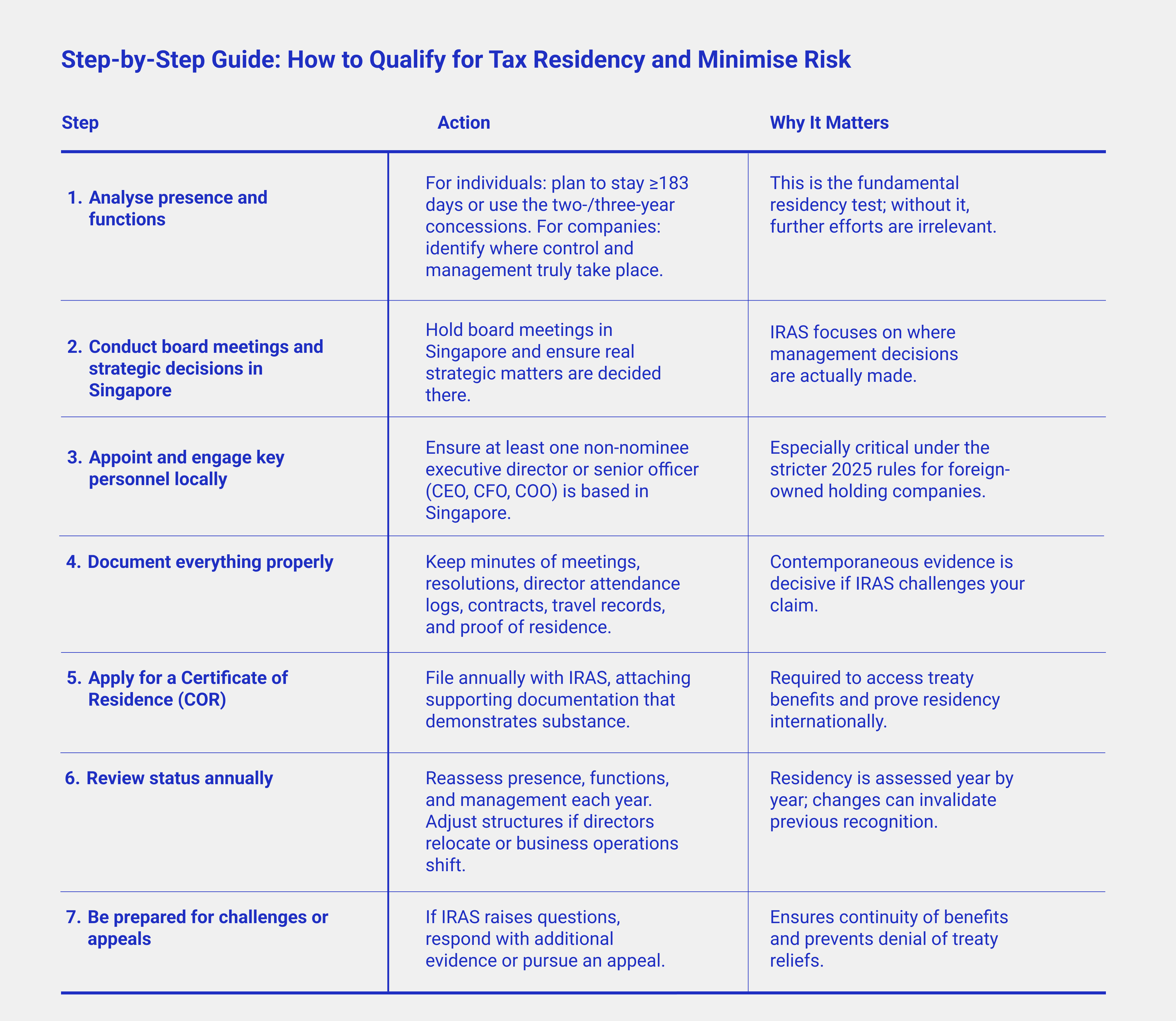

Corporate Tax Residency in 2025

Control and Management

For companies, residency is determined not by incorporation but by where control and management are exercised. According to IRAS, this refers to strategic decisions — the direction of the business, major investments, policies — and not to day-to-day operations.

Key indicators include:

Virtual board meetings are recognized, but only if at least half of the directors (or the chair) are physically in Singapore.

Certificate of Residence (COR)

A COR is issued by IRAS to certify residency for treaty purposes. Companies apply online, providing supporting documents such as board minutes, director details, and proof of decision-making in Singapore. Processing generally takes two to three weeks, but residency must be reassessed every year.

Stricter Conditions from 2025

IRAS now applies stricter criteria for foreign-owned holding companies:

These changes align with Singapore’s broader commitment to international tax standards and reflect an expectation that residency must correspond with real economic presence.

For companies, residency is determined not by incorporation but by where control and management are exercised. According to IRAS, this refers to strategic decisions — the direction of the business, major investments, policies — and not to day-to-day operations.

Key indicators include:

- Location of board meetings and where decisions are formally recorded.

- Physical presence of directors when strategic choices are made.

- Whether senior management (CEO, CFO, COO) is based in Singapore.

- Whether related Singapore entities perform management functions.

Virtual board meetings are recognized, but only if at least half of the directors (or the chair) are physically in Singapore.

Certificate of Residence (COR)

A COR is issued by IRAS to certify residency for treaty purposes. Companies apply online, providing supporting documents such as board minutes, director details, and proof of decision-making in Singapore. Processing generally takes two to three weeks, but residency must be reassessed every year.

Stricter Conditions from 2025

IRAS now applies stricter criteria for foreign-owned holding companies:

- Reliance solely on related Singapore subsidiaries is no longer sufficient.

- At least one non-nominee executive director should be based in Singapore, or genuine management functions must occur locally.

- Without this substance, IRAS can refuse to issue a COR, limiting access to treaty reliefs and exemptions.

These changes align with Singapore’s broader commitment to international tax standards and reflect an expectation that residency must correspond with real economic presence.

Documentation and Compliance

Residency status can be challenged, and IRAS expects robust evidence. Companies should maintain detailed records of board meetings, travel schedules of directors, and supporting documents that show decision-making in Singapore. Individuals should keep travel logs, contracts, and proof of residence.

Importantly, residency is determined year by year. A COR or residency determination in one year does not guarantee recognition in the next.

Importantly, residency is determined year by year. A COR or residency determination in one year does not guarantee recognition in the next.

Practical Roadmap

For Individuals:

For Companies:

- Track presence meticulously and plan around the 183-day rule.

- Use the two- and three-year concessions where applicable.

- Retain documentation proving residence ties.

- Apply for a COR if treaty relief abroad is needed.

For Companies:

- Hold board meetings in Singapore and ensure strategic matters are discussed and decided locally.

- Appoint at least one executive director who is genuinely based in Singapore.

- Demonstrate that management functions are carried out in Singapore, not merely rubber-stamped.

- Apply for COR annually with strong supporting documents.

- Conduct yearly reviews to adapt if business structures change.

Looking Ahead

Tax residency in Singapore is moving closer to the global standard of substance over form. The era of paper arrangements is over: IRAS expects proof of real decision-making, real presence, and real management in Singapore.

For individuals, mobility and remote work create new complexities in day-counting. For companies, cross-border structures must be carefully aligned to avoid treaty denial and reputational risk.

The message is clear: residency is not a matter of convenience — it is a strategic asset that requires planning, documentation, and periodic reassessment.

Singapore remains one of the most attractive jurisdictions for individuals and businesses, offering low rates, extensive treaty networks, and clarity in rules. But in 2025, securing tax residency requires more than meeting minimal thresholds.

Individuals must plan their time and maintain strong evidence of residence. Companies must ensure that boardrooms — physical or virtual — reflect true decision-making within Singapore. And everyone must prepare to demonstrate substance to IRAS.

Handled properly, residency status can unlock significant tax benefits and international opportunities. Mishandled, it can expose taxpayers to unnecessary costs and regulatory challenges.

NB! The information provided in this article is for general informational purposes only and does not constitute legal advice. While we strive to ensure the content is accurate and up-to-date, it should not be relied upon as a substitute for professional consultation. For personalized advice or assistance with legal matters, please contact our specialists directly.

For individuals, mobility and remote work create new complexities in day-counting. For companies, cross-border structures must be carefully aligned to avoid treaty denial and reputational risk.

The message is clear: residency is not a matter of convenience — it is a strategic asset that requires planning, documentation, and periodic reassessment.

Singapore remains one of the most attractive jurisdictions for individuals and businesses, offering low rates, extensive treaty networks, and clarity in rules. But in 2025, securing tax residency requires more than meeting minimal thresholds.

Individuals must plan their time and maintain strong evidence of residence. Companies must ensure that boardrooms — physical or virtual — reflect true decision-making within Singapore. And everyone must prepare to demonstrate substance to IRAS.

Handled properly, residency status can unlock significant tax benefits and international opportunities. Mishandled, it can expose taxpayers to unnecessary costs and regulatory challenges.

NB! The information provided in this article is for general informational purposes only and does not constitute legal advice. While we strive to ensure the content is accurate and up-to-date, it should not be relied upon as a substitute for professional consultation. For personalized advice or assistance with legal matters, please contact our specialists directly.

How we can help:

Company Incorporation & Business Setup – We assist businesses with company registration, structuring, and licensing in Singapore, ensuring full compliance with ACRA and MAS regulations.

Corporate Tax & Compliance Advisory – We help businesses leverage corporate income tax rebates, deductions, and incentive schemes, ensuring tax efficiency and compliance

Regulatory & Licensing Assistance – We guide businesses through the process of obtaining sector-specific licenses and ensuring compliance with MAS, IRAS, and other regulatory bodies, minimizing operational risks.

Enterprise Financing & Grant Support – We help businesses access Enterprise Financing Scheme (EFS), Private Credit Growth Fund, and SkillsFuture grants, aligning funding opportunities with business growth strategies.

Company Incorporation & Business Setup – We assist businesses with company registration, structuring, and licensing in Singapore, ensuring full compliance with ACRA and MAS regulations.

Corporate Tax & Compliance Advisory – We help businesses leverage corporate income tax rebates, deductions, and incentive schemes, ensuring tax efficiency and compliance

Regulatory & Licensing Assistance – We guide businesses through the process of obtaining sector-specific licenses and ensuring compliance with MAS, IRAS, and other regulatory bodies, minimizing operational risks.

Enterprise Financing & Grant Support – We help businesses access Enterprise Financing Scheme (EFS), Private Credit Growth Fund, and SkillsFuture grants, aligning funding opportunities with business growth strategies.